New Financial Statement Governmental Fund Presentation for School District Clients

by Cristina R. Oropeza, CPA, Audit Manager

Posted on September 12, 2023

During this past year, our firm re-evaluated how the financial statements are compiled and decided to make a major change to how funds will be presented. In the past, all individual funds were presented (i.e. Title I Grants, Special Education Grants, Other Federal Projects, etc.). For fiscal year 2023 and going forward, individual funds will now be presented into the following presentation fund groupings:

General

General- Classroom Site

- Instructional Improvement

- Federal and State Grants

- Food Service

- Other Special Revenue

- Debt Service

- Adjacent Ways

- Bond Building

- Other Capital Projects

How will the funds be combined under the bolded fund groupings above?

- The General Fund will include funds 001, 545 and 570, as well as other funds determined during GASB 54 implementation (this year will be a good time to revisit GASB 54 determinations with your auditor). The Unrestricted Capital Outlay Fund (610) will now be presented in this fund with an unassigned fund balance. If there are restricted balances in fund 610, you will need to provide that information to your auditor to ensure that portion is presented as restricted in the financial statements.

- Federal and State Grants will include funds 100-499, as well as funds 050, 071 and 072 if your District has them.

- Other Special Revenue will include funds 500-599, 850 and 955.

- Other Capital Projects will include funds 650-699.

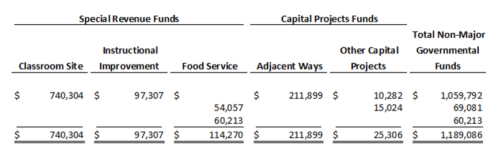

With this change, the financial statement report will be more condensed. Most of the changes you’ll see will be in the ‘Combining and Individual Fund Financial Statements and Schedules’ section of the report. You will no longer see combining statements for non-major special revenue funds, individual budget schedules for non-major special revenue funds, combining statements for non-major capital projects funds, and individual budget schedules for capital projects funds. Instead, you will see one combining balance sheet and one combining statement of revenues, expenditures and changes in fund balances that presents all non-major governmental funds – see example below. You will also see a budget schedule for only the fund groupings listed above.

With the new fund groupings and the removal of the statements and schedules mentioned above, the financial statement report will be shorter and provide a more meaningful presentation. Additionally, major funds are less likely to change each year which will make for a more meaningful comparison from year to year.

It is important to review the new fund groupings with your auditor. Management is ultimately responsible for the financial statements; therefore, understanding these new presentation fund groupings will be beneficial when reviewing and approving the financial statements. If you attended the 2023 Annual School District Conference, please refer to the presentation slides to aid in reviewing the financial statement groupings. If you have questions, please reach out to your auditor.

For a print-ready version: Click here