Indirect Costs – Fast Facts for Arizona School Districts

by Alex Cooksey, CFE, Consulting Manager

Posted on January 21, 2025

Indirect Cost Definition

Indirect Cost Definition

Indirect costs are expenditures that are necessary for an organization’s operations but are not easily associated with a specific grant project or program.

Indirect Cost examples include:

- Utilities

- Liability Insurance

- Employee salaries and benefits

- Administrative supplies

How do indirect costs relate to my school district?

When your district applies for a federal grant and is in the process of planning how those grant dollars will be spent, you may have noticed a budget line item that allows you to budget for indirect costs. If you are unaware of what indirect costs are, you probably skip over this line item. Does this sound familiar at all? If so, you may be missing out on recapturing resources for costs related to the administration and operation of a grant.

Grants are generally restricted to a specific purpose for which the funds may be expended on, and those costs are directly charged to the grant fund. However, there are other costs indirectly related to the administration of a grant recorded in other funds. For example, the district’s accounts payable department pays all vendor invoices no matter what the funding source. The district’s payroll department processes payroll for all employees whether they are coded under a specific grant or not.

This is where indirect costs come into play. The district may obtain an indirect cost rate to allow the grant to be charged a portion of these types of costs that are not easily traced directly to the grant.

How does your school district get an indirect cost rate?

Arizona school districts may obtain their indirect cost rates through the Arizona Department of Education (ADE) through the grants management department. This application is available through Grants Management Enterprise, ADE’s grants portal. The pathway to locate the section is below:

- Log into ADE Connect and navigate to the Grants Management application

- In the left blue menu, hover your cursor over Funding and then select Supplements

- Change the drop-down year to the funding year you are requesting your indirect cost calculation for

- Select the Indirect Cost hyperlink to access the section

Districts are required to populate the data sheet from their general ledger. The general ledger data used should be two years PRIOR to the year you are requesting an indirect cost rate. When you apply for indirect cost rates, you are applying for rates for the next funding year and need a full year’s worth of general ledger data. For example, if you are requesting the indirect cost rate for FY26 on January 20th, 2025, you would not be able to use your FY25 general ledger data because the year is only about halfway complete. You will need to pull your finalized general ledger data from FY24.

There are various ways districts can populate the information on the data sheet; by using reports and tools within the district’s ERP system or by manually locating each of the data sheet fields by filtering for each requested account code within the district’s general ledger. A district can request a restricted rate and an unrestricted rate be calculated. It is recommended to apply for both the unrestricted and restricted rates whether you plan to use both or not.

Once the data sheet is populated and approved by ADE, a restricted and unrestricted rate will be calculated. Unrestricted rates are used for grants where supplement not supplant is not applicable. Restricted indirect cost rates are used for certain grants that have specific statutory requirements that prohibit the use of federal funds to be used to supplant non-federal funds.

How does the General Ledger Impact the District’s Indirect Cost Rate?

ADE has created a guide to assist Arizona districts in how to map out their general ledger data to direct costs, indirect costs, and excluded/unallowed costs. The data sheet mapping guide can be downloaded at: https://gme.azed.gov/DocumentLibrary/ViewDocument.aspx?DocumentKey=2504430.0&inline=true (link verified as of 1/21/2025).

The data sheet map indicates which functions and object codes are labeled as indirect, direct, or unallowed for both the restricted and unrestricted rates. As mentioned previously, your district can decide whether to create reports that mirror the data sheet mapping provided by ADE to run the data from your ERP system or you can use the mapping provided by ADE to filter through your district’s general ledger to extract the data yourself. It’s important that your district utilizes the appropriate function and object codes for expenditures to ensure that your direct and indirect costs are properly allocated to calculate your indirect cost rates.

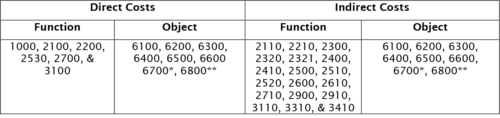

Account codes utilized for the unrestricted indirect cost rate calculation:

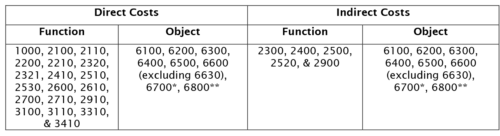

Account codes utilized for the restricted indirect cost rate calculation:

Account codes excluded from both rates:

- Food Expenditures – Object code 6630 – All Functions

- Capital Expenditures – Object code 6700 – All Functions (*Note: only capital expenditures that meet the federal capitalization threshold, currently $5,000 and above)

- Debt Service Expenditures – Object code 6800 – All Functions (**Note: non-debt service related expenditures in 6800 may be included, such as 6810 and 6890)

- All expenditures coded to the following functions: 3200, 3300, 3400, 4000, 5000, & 6000

- Funds excluded: 575, 8xx, & 95x

When completing a grant reimbursement request for indirect costs, it’s recommended to execute the indirect cost journal entry based on year-to-date expenditures.

Example scenario:

The district received a restricted indirect cost rate of 8% for the year

BUDGET

- Total grant allocation was $108,000

- Indirect cost budget was approved at $8,000

- Other directly related budgeted areas added up to $100,000

ACTUAL

- The district did not fully spend the $100,000 of directly related costs and only spent $80,000.

In this example, the district cannot request for reimbursement the full amount of indirect costs budgeted for since the full amount of directly related costs was not expended. The amount spent was $80,000 and that multiplied by the indirect cost rate of 8% results in $6,400 that can be charged to the grant for indirect costs.

Please note that some grants have additional factors that may disallow certain direct costs like capital expenditures to be factored into the total amount of indirect costs that can be charged to the grant.

Other Important Factors to Note:

- Grants that are state-funded generally do not allow for indirect costs

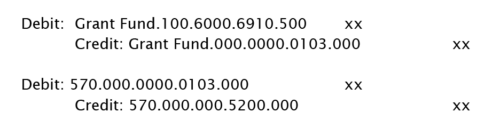

- Example indirect cost journal entry for Arizona school districts:

Print-ready version: Click here