Goals and Objectives of Governmental Financial Statements

by Mike A. Hoerig, CPA, Audit Partner

Posted on June 24, 2024

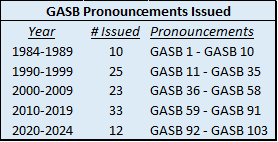

Governmental financial statements are unique in the world of accounting, and the recent flurry of new accounting pronouncements has added to the uniqueness. For perspective, the Governmental Accounting Standards Board (GASB) has issued 13 pronouncements in the last five years, and 32 since 2014 (see a full history of GASB statements in the chart). While not every pronouncement impacts every government, many in the last ten years have required countless hours and resources to assess and implement. As GASB celebrates its 40th year of standard setting, it may be a good time to re-focus and remember the primary goals and objectives of governmental financial statements.

Governmental financial statements are unique in the world of accounting, and the recent flurry of new accounting pronouncements has added to the uniqueness. For perspective, the Governmental Accounting Standards Board (GASB) has issued 13 pronouncements in the last five years, and 32 since 2014 (see a full history of GASB statements in the chart). While not every pronouncement impacts every government, many in the last ten years have required countless hours and resources to assess and implement. As GASB celebrates its 40th year of standard setting, it may be a good time to re-focus and remember the primary goals and objectives of governmental financial statements.

Purpose

For any organization, financial statements are a communication method to inform stakeholders about the resources and obligations of the entity. The financial statements and footnotes, and even the nonfinancial data that accompany them, allow users to gain a better understanding of the government’s operations, and draw conclusions about financial health and constraints faced. Especially in the government sector, financial statements also demonstrate the government’s duty to be publicly accountable.

Users and Uses

Generally, the groups to which governments are accountable can be separated into three categories: a) citizens, taxpayers, and service recipients; b) oversight bodies and grantors; and c) investors and creditors. Financial statements can also be useful to internal parties such as managers and directors, as well as the governance board.

Generally, the groups to which governments are accountable can be separated into three categories: a) citizens, taxpayers, and service recipients; b) oversight bodies and grantors; and c) investors and creditors. Financial statements can also be useful to internal parties such as managers and directors, as well as the governance board.

There are a number of reasons these groups might rely on the financial statements. Comparisons to adopted budgets might indicate where additional resources are needed, or where resources can be re-allocated. Financial statements might also be used to determine compliance with regulatory guidance, debt covenants, or grantor requirements. In some instances, financial statements might also demonstrate the efficiency or effectiveness of programs within the government. Understanding who the users are and how the financial information is relevant to each group should be considered when drafting any financial report.

Objectives

For effective communication of financial information, GASB has identified the following basic characteristics of governmental financial reporting.

Understandability

Information should be stated in the simplest terms (when possible) to facilitate comprehension by users of varying governmental experience. However, financial reporting should not exclude information merely because it is difficult to understand or because some users choose not to use it. Financial statement footnotes can aid in comprehension by providing additional details, background, and assumptions used by management to develop the financial report.

Reliability

Information in the financial statements should be verifiable, avoid bias, and faithfully represent the government’s operations. Additionally, the financial statements should be a complete representation and not omit items of qualitative or quantitative significance. Despite these goals, there are instances where estimates may be necessary, especially when precision is not cost-effective. However, in those situations, the financial statement footnotes should alert users to the estimate techniques used.

Relevance

Financial information is considered relevant if it is useful for a decision-maker who relies on the financial statements. This is a broad concept that might seem difficult to achieve due to the number of different users and uses, but adherence to the other financial statement characteristics typically helps ensure the relevance of the financial statements.

Timeliness

Financial information is most effective at communicating the government’s position when it is presented timely, and its usefulness to decision-makers decreases as time passes. As such, in some instances, a timely presentation of reasonable and accurate estimates is more useful to readers than trying to calculate more precise numbers that delay the issuance of a financial report.

Consistency

The underlying accounting principles, assumptions and estimates should be consistently applied from period to period to help decision-makers identify trends over multiple years. Changes in approach that could influence decision-makers should be sufficiently identified in the financial statement footnotes to maintain effective communication of the government’s operations.

Comparability

Information should be presented in a manner that is similar to other governments. While differences will always exist between governments (both in the amounts presented and functions performed), those differences should be due to substantive differences in the transactions presented or the governmental structure, and not due to the use of uncommon accounting procedures or practices.

Financial statements are an essential tool used to communicate a government’s operations, outcomes, and financial health; and that communication is most effective when the objectives above are considered. While it can be easy to get bogged down in the intricacies and nuances of new pronouncements, keeping these basic characteristics in mind can help ensure financial reports achieve their primary objectives – accurate, complete, and timely communication.

Print-ready version: Click here