GASB Statement No. 100 – Part II

by Christopher W. Heinfeld, CPA, Audit Partner

Posted on June 4, 2025

In the previous article here, we discussed an overview of GASB Statement No. 100. However, in this article, we will focus on the logistics of a change within the financial reporting entity caused by a change in major funds, and the awkwardness of reporting such.

According to GASB Statement No. 100, “A change to or within the financial reporting entity should be reported by adjusting the current reporting period’s beginning net position, fund balance, or fund net position, as applicable, for the effect of the change as if the change occurred as of the beginning of the reporting period.” Therefore, to meet this requirement, all reporting units (or columns) that appeared in the prior fiscal year financial statements will need to appear in the same respective current fiscal year financial statements. This should occur even if it only illustrates that the beginning balances are moving from one reporting unit (or column) to another, as is the case for a change in a fund’s presentation as major or nonmajor.

The nuance of this means reporting all major funds of the prior fiscal year financial statements in the current fiscal year financial statements, even if the funds are now nonmajor funds. This may result in funds being reported in two different statements. The reporting of prior fiscal year major funds that are current fiscal year nonmajor funds, is being referred to as ghost columns, as these columns would only contain a prior fiscal year ending balance (or “beginning balance, as previously reported”), and an adjustment to equal that amount (or “adjustment to beginning balances”), to arrive at a zero beginning balance (or “beginning balance, as restated”); the ghost columns will not include any activity for the current fiscal year.

The purpose of this is to ensure that the column’s beginning balances agree with the prior fiscal year’s respective financial statements. However, it is important to note that no ghost columns will be presented in position statements (ex. governmental funds balance sheet). Although the display of this approach is not illustrated in GASB Statement No. 100, the GASB has recently issued Implementation Guidance Update-2025 as an exposure draft, which includes confirmation that this display of the financial statements was the intention in GASB Statement No. 100. The GASB intends to finalize the Implementation Guidance Update-2025 by the end of June 2025.

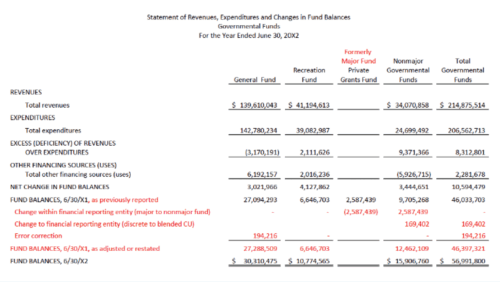

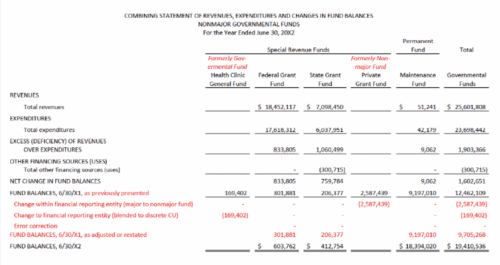

Below is an illustration provided by GFOA of how ghost columns may appear in the governmental funds statement of revenues, expenditures, and changes in fund balances, along with a corresponding combining statement of revenues, expenditures, and changes in fund balances for nonmajor governmental funds.

While you prepare and review your financial statements, some extra time may be necessary to ensure that the appropriate columns are listed on each financial statement, including ghost columns when necessary.

Print-ready version: Click here