Do I Need To Do a December Budget Revision?

by Alex Cooksey, Senior Associate

Posted on November 8, 2022

You may be sitting in your office thinking, “Now what…do I really get a break?” You just submitted the many required reports to meet the October 15th deadline but are unsure of where to go from here. Now that you have closed out the prior fiscal year, what should you be working towards?

You may be sitting in your office thinking, “Now what…do I really get a break?” You just submitted the many required reports to meet the October 15th deadline but are unsure of where to go from here. Now that you have closed out the prior fiscal year, what should you be working towards?

There are various upcoming deadlines, but in this article, we are going to focus in on the December budget revision process. There are many districts who find themselves wondering if doing one is even necessary, if not required by ADE.

If ADE doesn’t require the District to do one, you may ask yourself, what is the point in putting in extra time to do a revision? Let’s start with the facts and important information to remember about the December budget revision:

- December budget revisions are due to ADE Common Log on by December 15th

- The District is required to post a public hearing notice 10 days before the board approves the revised budget. Depending on your Governing Board Meeting schedule, this likely requires your budget to be published right about the same time you are pulling your turkey out of the oven. Why not spend the six hours it takes your bird to cook to revise your school district’s budget!

- ADE published the BUDG25 Expenditure analysis letter on Friday, November 4th. This letter indicates if a December revision will be required by the District based on the September BSA-55 report.

- The BUDG25 Expenditure Report is published monthly starting in September of each year. This report is used to inform the District of any comparisons between the District’s most recently approved budget to what ADE has calculated for the District’s budget based on ADM and other factors. Districts should use the BUDG25 as a tool to help with the revision process. At the end of this article, we have attached a sample BUDG25 report and listed out what each line item represents to help districts understand where their budget capacity is coming from.

There are many reasons a district may choose to revise their budget in December even when ADE does not require it. The list below includes some of the common reasons a district may revise their budget in December:

If Required by ADE:

- Pursuant to A.R.S. §15-905(E), if a district exceeds the General Budget or Unrestricted Capital budget that was allocated to the District by 1%, then a revision a required to reduce the allocated expenditures to be within the ADE calculated limits.

If not required by ADE, there are several reasons a district may choose to revise their budget. Some of those reasons include:

- Within the past few years, the budget forms have been finalized late in the year causing many districts to propose and/or adopt their budgets on draft forms that mirror the prior year’s budget forms. After the legislature approves the budget and the final forms are released, districts are given the option to revise their budget by September 15th to transfer their budget to the new forms and capture any legislative approved increase in funding. However, districts can always capture the legislative enacted budget variable during any revision up until the May 15th It is not recommended to wait that long on draft forms as the District would have gone nearly a full fiscal year of not having updated their budget with their Governing Board.

- Districts may revise the budget to update the budget balance carry forward from the prior year into the new fiscal year’s budget (as presented on the BUDG75).

- Districts may choose to revise their budget to reconcile with ADE’s calculations to make sure that the District always has the most up to date budget allocation.

- At the time of the adopted budget, if the District has not submitted all of the prior year completion reports for their grants, they would not be capturing carryforward grant allocations into their budget. If a district does have carryforward of any unused grant funds, they may want to revise their budget to capture the final grant allocations.

- Like grants, the District’s cash-controlled fund allocations may be uncertain at the time the District adopted the budget and, as the year progresses, it may become clearer on how much revenue is going to be received for the year.

- Governing Board members and the public place confidence that the District is staying on top of their budget numbers and revising the budget helps communicate the current budget position of the District.

There are several ways a district may approach the need to revise their budgets in December, and the reason for revision will vary by district and by year. Keep in mind once you have completed a December revision, it does not mean that you are required to now complete one every year thereafter. If not required by the previously mentioned exceeded budget limit, the purpose f or the December revision is to give the District an option to bring in their most up to date numbers to the community and Governing Board.

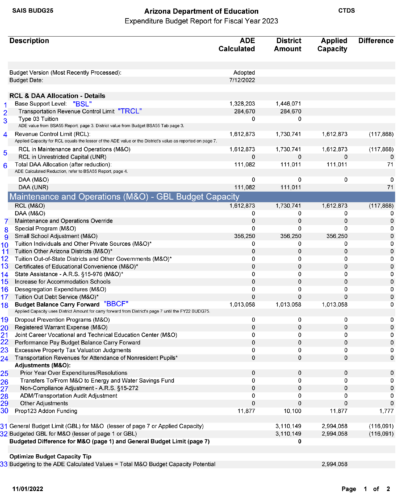

Within the BUDG 25, there are four columns of data.

- ADE Calculated – the amount calculated by ADE based on various sources such as ADM, transportation data, and budget data

- District Amount – this column represents the data from the District most recently approved budget and uploaded to ADE. The budget version and budget date are noted on the top of the BUDG25.

- Applied Capacity – this is the calculation applied to compare to the District Amount column. In most cases, this is the amount calculated by ADE.

- Difference – this is the mathematical calculation of the difference between the District Amount and the Applied Capacity. A negative reflects an over-budget amount on the District Amount and a positive amount reflects the additional budget capacity available to the District.

For all of the calculation amounts, if the field is available under both the M&O and Capital column, then the District has the option to allocate the budget capacity in either M&O or Capital.

BUDG25 Crosswalk

- The BSL is a complex calculation under ARS § 15-943 that calculates the base amount of budget capacity the District will receive. The calculation looks at the base support amount all districts receive, teacher experience index and student enrollment counts.

- The TRCL provides additional budget capacity for those districts who transport students. The calculation is based on prior year route miles and eligible students as calculated under AR. § 15-946.

- Type 03 Tuition is additional budget capacity allocated to an elementary school district that is not within a high school district for the high school students that live within their boundaries (Type 03). The budget formula adds this additional capacity for these students as they are not included within the original enrollment numbers in the BSL. This factor will be eliminated in FY24 as all students will be enrolled through open enrollment.

- The RCL is the sum of the BSL + TRCL + Type 03 Tuition plus any adjustments such as the audit fee adjustment.

- The District may choose to allocate out the RCL into either M&O (Fund 001) and/or Unrestricted Capital (Fund 610) based on their budgetary needs.

- The DAA Allocation is a calculation to provide districts with budget capacity for capital needs. Similar to the RCL, the District can allocate these funds to M&O and/or Unrestricted Capital.

- The Maintenance and Operation Override must be approved by voters and can increase the District’s budget capacity by up to 15% of the override calculated RCL.

- The Special Program Override must be approved by voters and can increase the District’s budget capacity by up to 5% of the override calculated RCL. It is important to note that the combined total of the M&O Override and Special Program Override cannot exceed 15%.

- The Small School Adjustment applies to districts with fewer than 125 students in K-8 or 100 or fewer students in grades 9-12. The District may request for additional budget capacity as needed under ARS § 15-949. The additional revenues are paid out through a tax levy.

- Tuition from Individuals accounts for the budgeted amount the District expects to receive for tuition from individuals and other private sources.

- Tuition from other Arizona districts accounts for the budgeted amount the District expects to receive for tuition from other Arizona districts.

- Tuition from Out-of-State Districts or other governmental entities accounts for the budgeted amount the District expects to receive for tuition from out of state Districts and other government entities.

- Certificates of Education Convenience are issued to students who do not live within a formal district boundary. Students, with their parents’ assistance, can apply for this certificate and submit to the District in the closest proximity. If approved as outlined under ARS § 15-825, the District will receive additional budget capacity which is funded by the County Superintendent.

- Additional budget capacity is allocated to districts who have students whose parents are employed by state institutions, state hospitals, and other instances listed under ARS § 15-976.

- If the District is an accommodation district, they may receive additional budget capacity.

- Additional budget capacity is allocated for districts that have a court ordered desegregation agreement with the United States Department of Education Office for Civil Rights under ARS §15-910. The capacity is only allowed to be captured by those who were involved in the original agreement and the District must request it every year. If a district does not include this in their budget in a given year, they are no longer allowed to receive it.

- This line item accounts for the tuition out debt service for the bond issues portion of the cost of tuition charged to Type 03 districts.

- The budget balance carry forward is all of the unutilized budget capacity that was carried forward from the prior year M&O budget balance.

- School districts which participated in the dropout prevention program as originally established pursuant to laws 1987, Chapter 333 and continued by Laws 1990, Chapter 399, may continue to budget for the dropout prevention program in an amount not to exceed the amount budgeted in fiscal year 1990-1991 (Laws 1992, Chapter 305, Section 32). Expenditures for programs serving grades 4 through 12 are allowed.

- Districts are permitted to add budget capacity for registered warrant or tax anticipation note interest expense incurred in FY21 (two prior years earlier) and sought ADE approval pursuant to ARS 15.910(N). This applies if the county treasurer pooled all District monies for investment and the District applied for early payments of their state aid apportionment or the District was not eligible for state aid.

- If the District has entered into an IGA to establish a jointly owned and operated CTED may increase their budget in accordance with ARS 15-910.01 This increase is only available for the first three years the CTED is created.

- Within the M&O fund only, a district can budget for performance pay expenditures. Fund 010 (Classroom Site Fund) budgeted expenditures do not apply here.

- District with excessive property tax assessed valuation judgments in accordance with ARS 42‑16213 and 42-16214 will increase their budget on this line item.

- School districts who establish an alternative transportation program in accordance with ARS 15‑923 add the budget capacity on this line item.

- If a district were to over-expend their budget in the prior year, the following fiscal year negative adjustment for the over expenditure will be reported here. This will reduce the current year budget by the over expenditure of the prior year.

- Within this line, districts will budget for the transfer to be made from the M&O Fund to the Energy and Water Savings Fund for the purpose of paying for capital investments to reduce energy costs.

- In the event the District is in non-compliance with the Uniform System of Financial records as listed in ARS § 15-272, ADE will identify the budget reduction approved by the State Board of Education.

- Within this line, ADE will adjust the budget capacity as a result of an ADM or Transportation audit. This can be an increase or a decrease to capacity.

- If any other adjustments are identified by ADE or adjustments required by the State Board of Education, they will be presented on this line item.

- Districts should budget for the additional capacity from Prop 123. Prop 123 funding came about as a result of restoring the inflation dollars that were withheld during the recession. This portion of funding is the District’s portion of the $75M of additional funding distributed across all public schools until 2025. The budget amount be allocated to M&O or Capital.

- The GBL is the lesser of the sum of all applied capacity noted in the BUDG25 or page 7 on the District’s current fiscal year budget.

- The budgeted GBL is the lesser of the GBL noted above on line 31 or page 1 on the District’s current fiscal year budget.

- This amount reflects the total M&O budget capacity potential based on all the prior line-item details. It’s the number the District should be allocating their M&O budget to.

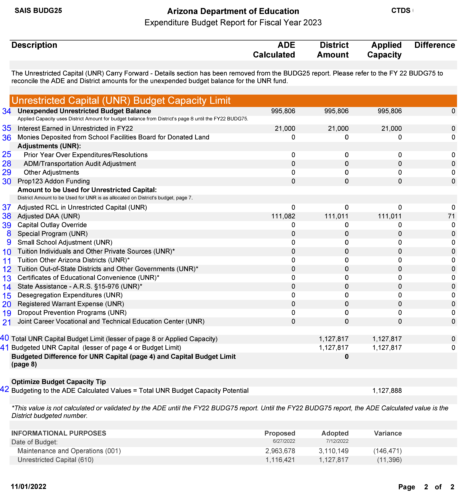

- The Unexpended Unrestricted Budget Balance accounts for the unexpended budget capacity from the prior year. Once the BUDG75 is issued, this amount will reflect the actual budget balance carryforward.

- This line item reflects the interest earned from Fund 610 in the prior fiscal year. The amount is added to the capital fund budget capacity.

- Any additional funding that was deposited by the SFB for donated land will be included in the budget limit.

- The amount that was allocated by the District in row 5 will populate within the Unrestricted Capital budget here. It is important to note that any increase in ADE calculated RCL will be allocated to the Unrestricted Capital Budget until the District revises the budget to allocate in M&O (if applicable).

- Adjusted DAA adds additionally budget capacity for districts with less than 600 students and must apply for the special adjustment as outlined in ARS § 15-963.

- Similar to an M&O Override, a Capital Override must be approved by voters and can increase the District’s budget capacity by up to 10% of the RCL.

- Similar to row 31 – The UNR Capital Budget Limit is the lesser of the sum of all applied capacity noted in the BUDG25 or page 8 on the District’s current fiscal year budget.

- Similar to row 32 – The budgeted UNR Capital Budget Limit is the lesser of the budget in row 41 or page 4 on the District’s current fiscal year budget.

- Similar to row 33 – This is the bottom-line budget number for the District. It’s the number the District should be allocating their Unrestricted Capital budget to.

The final portion of the BUDG25 is the “Informational Purposes” section. The section identifies the difference between the proposed and adopted budget limits. During the 2022 legislative session, the legislature passed session law to allow school districts to increase the adopted budget from the proposed budget to account for the increased per pupil funding and additional Group B add-on weights.

We hope this information is helpful to your District as you embark on the budget revision process!

For a print-ready version of this article: Click here