COVID-19 and the Changing Landscape of Single Audits

by Brittney Williams, CPA, CGFM, Audit Partner

Posted on March 14, 2022

What hasn’t changed in the last two years in the world? Audits and, in particular, Single Audits are no exception. With over $10.1 billion being granted to Arizona communities in federal award obligations, this marks the greatest influx of federal dollars into many of our state/local governments, not-for-profits and local businesses that many of us have ever experienced. With all of this new funding, the landscape has changed dramatically over the last two years relative to how single audits are performed for non-federal entities. The guidance and rules for spending and auditing these federal monies seems to change on a constant basis, creating challenges we have never encountered before during the audit process. Late addendum releases to the audit communities created delays in filing, new and interesting reporting requirements didn’t follow traditional time frames or structure, and more exemptions and waivers occurred than we typically see in a given year. These have all led to much confusion and a need to rapidly adapt to the new climate.

What hasn’t changed in the last two years in the world? Audits and, in particular, Single Audits are no exception. With over $10.1 billion being granted to Arizona communities in federal award obligations, this marks the greatest influx of federal dollars into many of our state/local governments, not-for-profits and local businesses that many of us have ever experienced. With all of this new funding, the landscape has changed dramatically over the last two years relative to how single audits are performed for non-federal entities. The guidance and rules for spending and auditing these federal monies seems to change on a constant basis, creating challenges we have never encountered before during the audit process. Late addendum releases to the audit communities created delays in filing, new and interesting reporting requirements didn’t follow traditional time frames or structure, and more exemptions and waivers occurred than we typically see in a given year. These have all led to much confusion and a need to rapidly adapt to the new climate.

One key item of Single Audits that has required significantly more attention in the past couple of years is the Schedule of Expenditures of Federal Awards (SEFA). Did you know that an accurate SEFA is crucial to ensuring a well-performed Single Audit? Whether you prepare the SEFA in- house or contract with your auditor to assist with the preparation, accurate record keeping is key. Inaccuracies in the SEFA can lead to the need to reissue the Single Audit report in cases where the proper major federal programs weren’t tested or proper coverage wasn’t obtained.

SEFA reporting has become much more complex and challenging in the last two years due to the influx of COVID-19 funding. New federal regulations for testing high risk programs coupled with the difficulty of properly identifying which funds are COVID vs. standard grants have led to significantly more time being spent on single audits, not to mention the difficulty of testing these funds when the guidance for allowability of spending and how to test these programs is released sometimes much later than the funds themselves. But that is a topic for another lengthy article!

There are many resources out there to assist in preparing a SEFA and understanding the different elements of the schedule. See AICPA SEFA Practice Aid for Auditees for a useful tool.

Not only has the tracking and testing of the federal grants changed significantly, but the reporting on the SEFA and the Data Collection Form submitted to the Federal Audit Clearinghouse annually has additional requirements. See table below for an example of proper presentation and breakout of COVID-19 monies.

Tracking of Personal Protective Equipment (PPE) donations have become an area of focus. Entities are now required to report the fair value of donated federally funded PPE at time of donation. This information should be reported in the notes to the SEFA, unless an Assistance Listing Number was provided. In that case, the amount will be reported on the SEFA, although this amount doesn’t affect major federal program thresholds or determinations.

Tracking subawards to pass-through entities has also changed this year. Not only are auditees required to report the amount of a federal grant passed through to a subrecipient on their SEFA, but in fiscal year 2021, the Office of Management and Budget (OMB) released a new requirement for reporting any funds in excess of $30,000 (under new Uniform Guidance) through the Federal Funding Accountability and Transparency Act (FFATA) Subaward Reporting Systems. The auditor will be required to test the FFATA reporting if the compliance requirement is applicable in the compliance supplement and determined to be direct and material to the major federal program. Auditees that are first tier (direct) recipients that pass more than $30,000 to a subrecipient will always be required to do the reporting. So far two programs are exempt from this reporting- Coronavirus Relief Fund and Coronavirus State and Local Fiscal Recovery Funds. (USASpending.gov for FFATA Reporting)

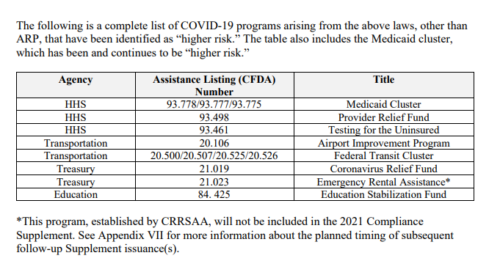

One key change in the fiscal year 2021 was related to the identification of certain federal programs as “higher risk” by the federal granting agencies. To summarize, the chart below indicates which programs were identified as “higher risk”. The auditor, in their assessment of these programs would need to determine if COVID-19 funding was material to the program. If it was, the auditor needed to test it as a major program in the current year, regardless of whether it met all of the other traditional requirements of a low risk program for the year. This changed the volume of testing major federal programs in fiscal 2021 for almost every audit. For example, if we tested the Education Stabilization Fund in fiscal year 2020 with no findings and the entity as a whole remained low risk, traditionally we could wait two years to test this program again. Under the new requirements, since Education Stabilization Funds are 100% COVID-19 funded, we will need to test this program every year, until the requirement changes.

Now that we have covered some of the challenges faced in the last few years, below are some tips and tricks for auditees to use when gathering information for SEFA preparation to ensure an accurate audit is performed and there is complete and proper reporting of grants to the Federal Government.

- Establish good internal controls to review all grant agreements and properly identify and track COVID-19 monies separately for SEFA purposes. Identify these separately on the SEFA.

- Keep track of “out of period” expenses – i.e., awards spent in a prior year and reported on the SEFA in the next fiscal year.

- Ensure you have the correct Assistance Listing Number and Name. (Official grant names by Assistance Listing Number)

- Review programs to determine if they are part of a “cluster” and need to be reported as such on the SEFA.

- Ensure that you have a complete listing of grant expenditures for the year.

- Reconcile federal revenues recorded in the general ledger to federal expenditures reported on the SEFA.

- Ensure strong communication between all departments (finance, grants, program directors, etc.).

- Ensure the alpha suffix is included after the assistance listing number for all applicable grants from the US Department of Education. (USDOE alpha suffix listing)

There are several unique requirements for reporting of federal expenditures on the SEFA and to the federal government associated with individual grant programs such as Provider Relief Fund and the Coronavirus State and Local Fiscal Recovery Funds. If these grants apply to your entity, be sure you are familiar with these requirements.

The AICPA recently released a new document for organizations subject to single audit requirements. This was done to the influx of COVID-19 federal funding into the economy and contains some very helpful tips and links to resources to ensure effective internal controls are being maintained with regard to the spending of federal monies. (AICPA Single Audit Tips for Auditees)

In light of all the changes mentioned above, it is strongly recommended to take the necessary time to educate and familiarize yourself with the various rules, regulations and waivers that have been and continue to be released for the different federal grants. Review all of the many resources listed in this article and the links provided. I hope they provide you with the knowledge you need to succeed in the ever changing single audit world we now live in.

For a print-ready version of this article: click here

Related articles:

Preparing for Your First Single Audit