GASB Standards Update

by Mike A. Hoerig, CPA, Audit Partner

Posted on July 14, 2021

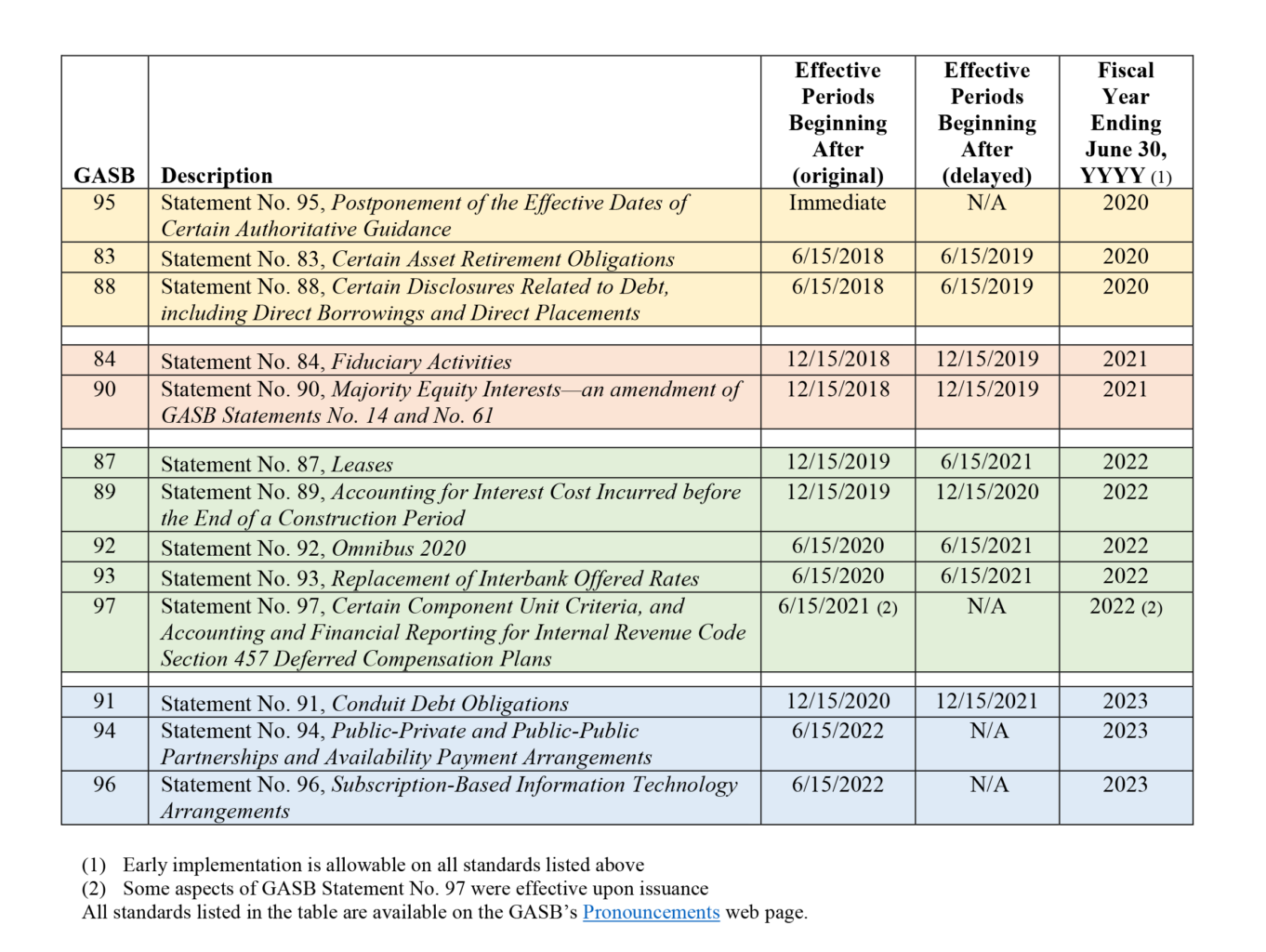

The Governmental Accounting Standards Board (GASB) has been, seemingly, busier in recent years researching, deliberating, and issuing a number of standards that will take effect in coming years. While some relief was provided with the passage of GASB Statement No. 95, Postponement of the Effective Dates of Certain Authoritative Guidance, in May 2020, the implementation period is already here (or quickly approaching) for a number of these standards. The table at the end of this article summarizes the standards that will be implemented soon – including their original effective dates, and the revised effective dates established by GASB Statement No. 95. Some of these standards could have a significant effect on governments, while others will have limited application for many governments.

The Governmental Accounting Standards Board (GASB) has been, seemingly, busier in recent years researching, deliberating, and issuing a number of standards that will take effect in coming years. While some relief was provided with the passage of GASB Statement No. 95, Postponement of the Effective Dates of Certain Authoritative Guidance, in May 2020, the implementation period is already here (or quickly approaching) for a number of these standards. The table at the end of this article summarizes the standards that will be implemented soon – including their original effective dates, and the revised effective dates established by GASB Statement No. 95. Some of these standards could have a significant effect on governments, while others will have limited application for many governments.

GASB Statement No. 87, Leases

Likely the most significant effect on governments will be the implementation of GASB Statement No. 87, Leases. By now you’ve undoubtedly heard about this Standard, and the multitude of ways it will change existing terminology and treatment for agreements previously referred to as “operating leases” and “capital leases”. The initial steps for implementation include identifying all potential agreements and contracts that could be impacted by the Standard – both from a lessee and lessor perspective. Once a “master list” of agreements has been developed, management should diligently research existing agreement language to determine the proper reporting classifications – lease, financed purchase, or something else. Note that, generally, agreements with a maximum potential term of 12 months or less are scoped out of the Standard. We highly recommend the use of a spreadsheet to summarize and track the key terms in each agreement: contract numbers, beginning and end dates, renewal options, termination clauses and dates, payment frequencies, interest rates, etc. Summarizing the key terms will help identify similarities across different contracts and aid in financial reporting consistency required by the Standard. Additionally, summarizing key terms will also ensure consistency in application from period to period and help identify expired contracts as they occur in future years.

GASB Statement No. 84, Fiduciary Activities

Another standard with a more immediate impact, but probably requiring less research, is GASB Statement No. 84, Fiduciary Activities. This Standard updates existing fiduciary activity guidance, eliminates the presentation of agency funds, and substitutes a new custodial fund definition. Custodial funds are generally defined as assets that are controlled by the government; are not derived from the government’s own-source revenues, or government-mandated and voluntary nonexchange transactions; and the assets held are not for the benefit of the government, and can’t be used to satisfy the government’s creditors. Management should review existing agency funds and determine if they continue to meet the new fiduciary definition and, if not, determine the proper reporting method for funds previously-classified as agency funds.

Other Pronouncements

There are a number of other standards in the table below that should be read and analyzed to determine their potential impact. GASB Statement No. 92, Omnibus 2020, addresses several topics – including the guidance in GASB Statement No. 84 and Statement No. 87 – as well as various technical corrections in other standards and guidance. Additionally, GASB Statement No. 97, Certain Component Unit Criteria, and Accounting and Financial Reporting for Internal Revenue Code Section 457 Deferred Compensation Plans, could impact many governments that offer deferred compensation plans. GASB Statement No. 97 also provides guidance for certain fiduciary component units and defined contribution benefits provided by governments.

Aside from the standards already issued, GASB continues to research a number of other topic areas. The most significant projects include revamping the revenue and expense recognition criteria and the financial reporting model. These comprehensive projects are in various stages of deliberation and will likely take effect for fiscal years beginning after June 15, 2024 and later. There are also several practice issue projects in various phases of research and deliberation. A complete list of all GASB projects can be viewed here.

For a print-ready version of this article: Click here